Lowest food inflation in 17 months

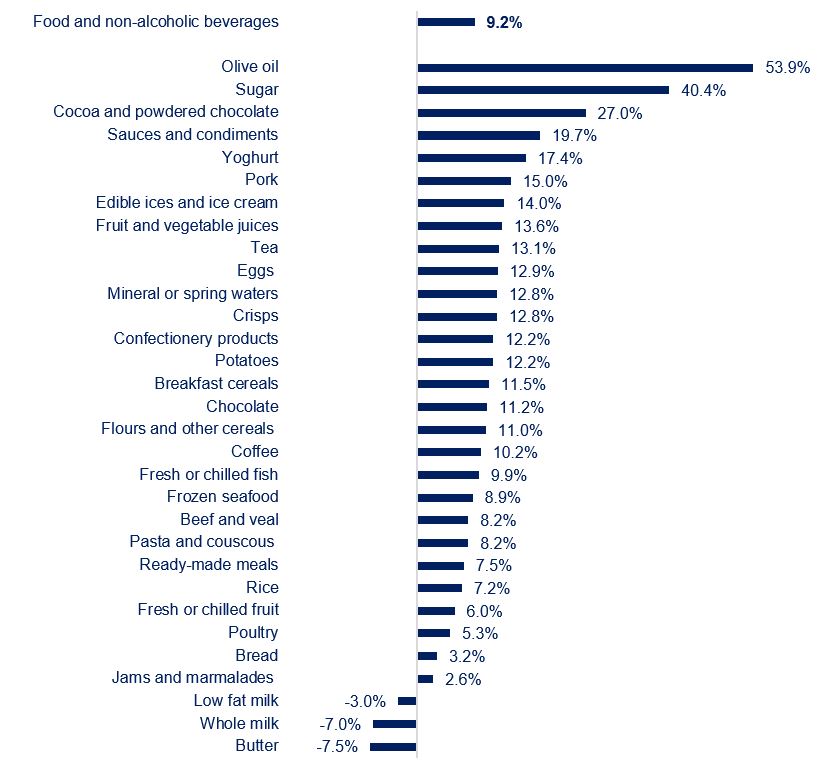

November food and non-alcoholic drink prices rose by 9.2% year on year, a slower rise than October’s 10.1% increase. November was the eighth month of easing food and non-alcoholic drink inflation and the lowest rate since May 2022. On the month, prices increased by 0.3%, following a 0.1% monthly rise in October.

Topics

By category, there are significant differences between products. Year-on-year inflation has been slowing for 29 categories out of the 49 main categories reported by the Office for National Statistics (ONS). That compares with 36 categories the previous month. Butter and whole milk continue to see significant price drops, of 7.5% and 7.0%, respectively (see chart). Olive oil and sugar saw another massive acceleration in inflation in prices in November, of 53.9% and 40.4%, respectively. Droughts in European countries producers of olive oil and the El Nino significantly impacted the worldwide output of both commodities.

Food and non-alcoholic drink year-on-year inflation by category (Nov-23 compared to Nov-22)

Source: ONS

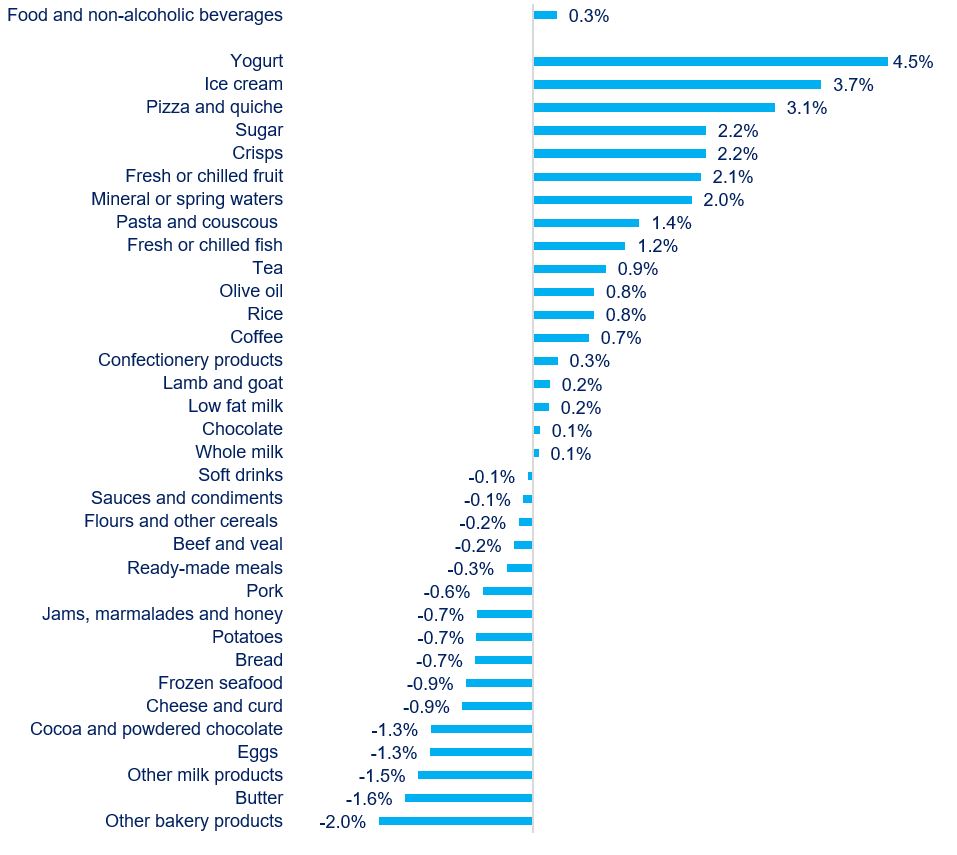

On the month, prices fell for 23 categories out of the 49. Butter was 1.6% cheaper than in October, and eggs 1.3%. The highest monthly rises were recorded by yogurt (4.5%) and ice cream (3.7%) (see chart).

Food and non-alcoholic drink month-on-month inflation by category (Nov-23 compared to Oct-23)

Source: ONS

On the producer side, some costs are falling. UK-sourced ingredients were 2.5% cheaper compared to a year ago, but 0.2% more expensive on the month, a third consecutive month of price rises. Imported ingredients were 8.1% more expensive on the year, and 0.6% on the month. Overall costs facing food and drink manufacturers fell by 0.7% on an annual basis, but rose by 0.1% on the month.

Some fresh inflationary pressures have been arising recently. The recent navigation turmoil in the Red Sea pushed global shipping rates up by 10% since the start of the month, which will put upward pressures on the cost of imports. In addition, oil and energy costs will also be impacted, as much of Europe’s gas is shipped, which, in turn, will add to inflationary pressures in the industry.

While persistent labour shortages and the rise in the minimum wage rates in April 2024 will continue to push costs up, undoing some of the gains from the declining prices of some inputs.

On the global commodity markets, there have been some new developments. Sugar prices fell over the last three weeks by about 20%, mainly due to India’s move to ban the use of sugarcane syrup or juice in ethanol production. Nonetheless, India has a target for biofuel blending, which means it might have to resort to using other grains for ethanol, risking pushing some other prices up. UN global food index held steady in November, with prices of vegetable oils and dairy higher in November from October. Over global food prices are 25% below their March 2022 peak, but remain about 21% above their February 2020 level.

This is indicative of the fact that the impacts of the recent price pressures have been so large and interconnected that they’re still taking some time to filter through into final consumer prices. While new developments will mean that food inflation will remain persistent for the coming months, albeit with the annual rate continuing to slow.

Manufacturers have absorbed a significant share of the recent cost rises. To be able to invest, they need to rebuild their margins. However, with grocery volumes in decline and a notable shift to cheaper products, it’s unlikely they’ll be able to increase either prices or sales volumes, leaving them between a rock and a hard place.

That’s why manufacturers are prioritising innovation more than ever, with 81% of them, up from 54% in Q2, focusing on new product development, as developing new products helps maintain competitive advantage. All large businesses and most (91%) mid-size companies stated they are developing new products. The industry is tackling a variety of ways to support growth: 42% of businesses also aim to restructure operations and 39% seek to adapt and/or simplify their supply chains, and 41% plan to increase their capital investment expenditure in the next 12 months.

In the wider economy, the annual CPI inflation rate slowed to 3.9% down from 4.6% in October. Core inflation – a measure closely watched by the Bank of England as it excludes more volatile items such as food and energy and considered a better measure of underlying inflation, has eased to 5.1% down from 5.7 in October.

Inflation easing is good news, although it’s still above the Bank of England target of 2.0%. At their last December meeting, the Bank kept interest rates unchanged at 5.25%. While markets are projecting some rate cuts for 2024, the Bank has warned that might take a while. For besides easing inflationary pressures, the Bank is mainly following pay rises. Wages have been surpassing the inflation rate in recent months. Following 19 months of real pay declines, over the last four months to October real pay crossed into positive territory. The main question is whether the main driver of these pay rises have been workers bargaining for higher wages as a response to the cost of living crisis or a tight labour market. If the latter, inflation is likely to persist for longer and, alongside, potentially unchanged rates.

For the industry to recover its resilience after the shocks of recent years, we need the government urgently to review the conditions for investment in our sector. Improving existing and planned regulation that is adding avoidable costs to the industry would help, from Extended Producer Responsibility, the Plastics Packaging Tax and ‘Not for EU’ labelling.